Why That Lump-Sum Mortgage Payment is Your Secret Weapon (If You Play It Right)

ONTARIOHOUSINGREAL ESTATEINTEREST RATESMORTGAGES

Matthew Maingot

6/30/20259 min read

Why That Lump-Sum Mortgage Payment is Your Secret Weapon (If You Play It Right)

Picture this: You check your bank account, post-tax refund or yearly bonus, and suddenly the possibility of making a dent in your mortgage feels real—not just something your parents' friends talk about at backyard BBQs. But is it always wise to toss your extra cash at the mortgage, or could there be smarter moves? Let’s break through the jargon and look at real-life tactics (mishaps included) that everyday Canadians use to get mortgage-free sooner.

Throwing Down Extra Cash: The Art & Science of Lump-Sum Payments

If you’ve ever stared at your mortgage statement and wondered if you’ll ever see the end of it, you’re not alone. With balances often in the hundreds of thousands, it can feel like you’re running a marathon in slow motion. But here’s a secret weapon many homeowners overlook: the lump-sum payment. When used wisely, these extra mortgage payments can help you pay off your mortgage early and rack up serious mortgage interest savings—even if you’re not rolling in cash.

Why Even Small Lump-Sum Payments Matter

Let’s break it down. A lump-sum payment is a one-time extra payment you make directly toward your mortgage principal. Unlike your regular payments, which cover both interest and principal, a lump-sum goes straight to chipping away at what you actually owe. The result? You immediately reduce the amount of interest you’ll pay for the rest of your mortgage. Over time, the compounding effect of these savings can be huge.

Research shows that even modest annual lump-sum payments—say, 5% to 10% of your original mortgage principal—can significantly reduce mortgage debt faster and save you thousands in interest over the life of your loan. Most closed mortgages in Canada allow you to make lump-sum payments up to 10% of the principal each year without penalty, but always check your lender’s rules.

Real-Life Impact: Patty Hopper’s Story

Patty Hopper, a mobile mortgage specialist at Vancity, sees the benefits firsthand. She recalls how one client used a work bonus as a lump-sum payment and was stunned by the results. “Making lump sum payments on your mortgage is a pretty powerful strategy to save on your interest and become mortgage free a lot sooner,” Hopper explains. The client’s single bonus payment translated into thousands saved in interest and a shorter amortization period. That’s the kind of statement shock you want: less interest, more progress.

The 2025 Twist: Higher Rates, Bigger Savings

Here’s where things get even more interesting. Back when mortgage rates were under 2%, the case for making extra mortgage payments wasn’t always clear-cut. Some people preferred to invest extra cash, hoping for higher returns. But in 2025, with rates hovering around 5% or more, the math has changed. Every dollar you put toward your mortgage now delivers a guaranteed return—by slashing the interest you’d otherwise pay. As Mengdie Hong, a senior financial planner at RBC, puts it: “If your mortgage rate is higher than what you expect from your investment … it may be best to allocate this excess cash to the mortgage.”

Myth-Buster: Lump-Sum Payment Benefits Aren’t Just for the Wealthy

Think lump-sum payments are only for the rich? Not so fast. Financial experts say windfalls like work bonuses, tax refunds, or even a small inheritance can all be put to work. “Any little bit is going to save you interest,” Hopper says. Even if you can only manage a lump-sum payment once a year, the benefits add up. And if you’re worried about flexibility, Hong advises reviewing your full financial picture—emergency fund, RRSP, other debts—before making a move. The goal is to balance debt reduction with financial flexibility.

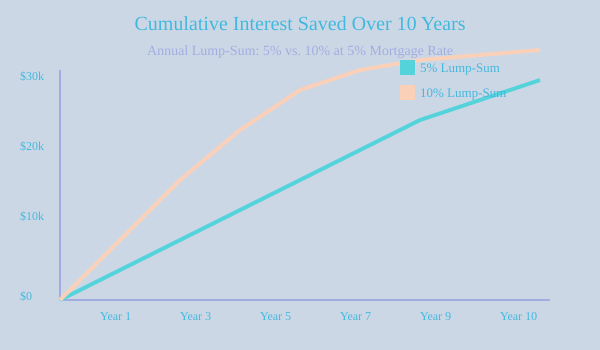

‘Aha!’ Data Point: The Outsized Impact of 5-10% Payments

Here’s a quick data check: If you make annual lump-sum payments of 5% or 10% of your principal, you could save thousands in interest and shave years off your mortgage. The effect is even more pronounced at today’s higher rates. And if you ever sell your home before the mortgage is up, a lower balance means more cash in your pocket for the next chapter.

“Making lump sum payments on your mortgage is a pretty powerful strategy to save on your interest and become mortgage free a lot sooner.” – Patty Hopper, Vancity

There’s also a psychological win here. Every extra payment brings you closer to full ownership and the peace of mind that comes with being debt-free. Once, I made a lump-sum payment with a small bonus, and the statement shock was real: less interest, more progress. It’s a feeling that sticks with you.

Chart: Cumulative Interest Saved with Annual Lump-Sum Payments

Secrets, Traps & Loopholes: When Lump-Sum Payments Aren’t So Simple

Making a lump-sum payment on your mortgage sounds like a straightforward way to slash your debt and save on interest. But before you rush to put that tax refund or work bonus onto your mortgage, it’s crucial to understand the maze of lump sum payment restrictions and the fine print that comes with most home loans in Canada. The reality? Not all mortgages treat extra payments equally—and sometimes, the “secret weapon” of a lump-sum payment can backfire if you’re not careful.

Closed Mortgage? There’s a Limit

If you have a closed mortgage, you’re not alone—most Canadians do. But here’s the catch: closed mortgages typically come with mortgage prepayment restrictions. Most lenders allow you to pay only 10-20% of your original principal each year as a lump sum without penalty. Go over that limit, and you’ll trigger penalty fees for prepayment—sometimes hefty enough to wipe out the interest savings you were hoping for.

It’s all spelled out in your mortgage contract, usually buried in legalese that’s easy to gloss over. But don’t ignore it. As Patty Hopper, a mobile mortgage specialist at Vancity, puts it, “Any little bit is going to save you interest,” but only if you stay within your lender’s rules. Exceeding your annual allowance? That’s when the dreaded mortgage payment penalty comes into play, and the math can surprise you—in a bad way.

Open Mortgage Option: More Freedom, Higher Cost

Maybe you’re thinking about an open mortgage option instead. Open mortgages let you make unlimited lump-sum payments or even pay off your entire balance at any time, penalty-free. Sounds perfect, right? The trade-off is that open mortgages almost always come with higher interest rates. So, while you gain flexibility, you might end up paying more in interest over the life of your loan. It’s a classic case of paying for freedom.

Research shows that for most homeowners, the extra interest on an open mortgage outweighs the benefit—unless you’re planning to pay off your mortgage very quickly or expect a significant windfall.

Renewal: The Wild Card

Here’s a loophole many miss: mortgage prepayment restrictions often disappear when your mortgage comes up for renewal. That’s your window to make a larger lump-sum payment without penalty. But timing is everything. If you miss the renewal window, you’re back under the old rules. It’s worth marking your calendar and planning ahead if you want to maximize your prepayment without triggering fees.

Penalty Fees vs. Long-Term Savings: Do the Math

It’s tempting to focus on the immediate satisfaction of making a big dent in your mortgage. But sometimes, the numbers don’t add up the way you expect. If you exceed your allowed prepayment and pay a penalty, will you actually come out ahead in the long run? Sometimes yes, sometimes no. Using a mortgage payment calculator can help you compare the cost of penalty fees prepayment against the interest you’d save by reducing your balance. The answer isn’t always obvious—and sometimes, it’s not in your favour.

Don’t Act in a Vacuum: Consider Your Whole Financial Picture

Before you make any lump-sum payment, step back and look at your entire financial landscape. Do you have high-interest credit card debt? Is your emergency fund topped up? Are you contributing to your RRSP or TFSA? Financial planner Mengdie Hong of RBC advises, “So before you apply this lump sum, you may want to review all the debts that you have.” Sometimes, paying down higher-interest debt or investing for a higher return makes more sense than prepaying your mortgage.

In simple words, if your mortgage rate is higher than what you expect from your investment … it may be best to allocate this excess cash to the mortgage, but if your expected return is noticeably higher than the mortgage, you may want to invest. – Mengdie Hong, RBC

Flexibility and liquidity matter, too. As Hong notes, “We always want to have flexibility and options in our financial plan.” Don’t drain your savings just to pay down your mortgage faster if it leaves you vulnerable to unexpected expenses.

The Fine Print Isn’t Just Decoration

Finally, don’t underestimate the importance of reading your mortgage documents. The lump sum payment restrictions and mortgage prepayment options are all spelled out there, even if the language is dense. If you’re unsure, ask your lender or broker to walk you through the details. The fine print can make the difference between a smart financial move and an expensive misstep.

2025 Canadian Reality Check: Renewal Shocks and Future-Proofing Your Mortgage

Let’s be honest—2025 isn’t shaping up to be an easy year for Canadian homeowners. If you’re staring down a mortgage renewal, you’re probably feeling the pressure. Mortgage renewal rates are climbing, and the term “mortgage renewal shock” is popping up everywhere for good reason. After years of ultra-low rates, many Canadians are now facing the reality of higher monthly payments. The numbers tell the story: households took on a staggering $9.1 billion in new mortgage debt in April 2025 alone. That’s a clear sign the market is shifting, and it’s time to get strategic about your mortgage payment strategies in Canada.

So, what can you do to future-proof your finances against these rising costs? One of the most effective mortgage prepayment strategies is making a lump-sum payment before your renewal. It’s not just about feeling good—it’s about math. When you put extra cash toward your mortgage principal, you immediately reduce the amount you owe. That means less interest accumulating over time and, crucially, a lower balance when your mortgage comes up for renewal. In a climate where mortgage renewal rates are higher than they’ve been in years, that can cushion the blow and help you avoid a nasty payment hike.

Financial experts across Canada agree: if you’re lucky enough to have extra cash—maybe from a work bonus, a tax refund, or even a small windfall—consider putting it toward your mortgage. As Patty Hopper, a mobile mortgage specialist at Vancity, puts it, “Making lump sum payments on your mortgage is a pretty powerful strategy to save on your interest and become mortgage free a lot sooner.” Even a modest lump-sum payment can make a real difference, especially when rates are rising. And if you’re planning to sell your home, that extra payment can mean more cash in your pocket for your next move. Hopper sums it up:

“You’ve got more cash on hand to make your next purchase or to move forward in the next leg of your journey.”

But don’t forget—mortgage prepayment strategies aren’t one-size-fits-all. Lenders have rules about how much you can pay down each year without penalty. Most closed mortgages let you pay up to 10% of the principal annually, while open mortgages offer more flexibility but often come with higher rates. Always check your mortgage agreement or talk to your lender before making a move. And remember, these prepayment privileges often reset at renewal, so timing matters.

Now, you might be tempted by the idea of a mortgage amortization extension. Extending your amortization can lower your monthly payments, which sounds great if you’re feeling squeezed. But here’s the catch: you’ll pay more in interest over the life of your loan. It’s a double-edged sword—short-term relief, long-term cost. Research shows that while this option can help with immediate cash flow, it’s not always the best route if your goal is to save money overall. Weigh your options carefully, and consider using a mortgage payment calculator to see how different scenarios play out. Sometimes, the peace of mind from lower payments is worth it; other times, you’re better off tightening your belt and paying down the principal faster.

Of course, lump-sum payments shouldn’t come at the expense of your overall financial health. Before you put extra money toward your mortgage, check in on your emergency fund, retirement savings, and any high-interest debts. As Mengdie Hong, a senior financial planner at RBC, advises, “We always want to have flexibility and options in our financial plan.” If you’re carrying credit card debt or other loans with higher rates, tackle those first. But if your finances are in good shape, making a lump-sum mortgage payment can be a smart, future-proof move.

In the end, the best mortgage payment strategies Canada has to offer are the ones tailored to your unique situation. Rising rates in 2025 mean it’s more important than ever to plan ahead, use mortgage calculators, and talk to your lender. Whether you’re bracing for a mortgage renewal shock or just looking to pay off your home faster, every extra dollar counts. The satisfaction of being prepared—less debt, more choices, and a smoother path forward—is well worth the effort.

TL;DR: Lump-sum mortgage payments can save you thousands and years, especially in a high rate market—but always weigh restrictions, penalties, and your broader financial health before pulling the trigger. Plan, compare, and remember: there isn’t a one-size-fits-all solution.

Growth

Empowering clients through personalized mortgage solutions.

Service:

info@matthewmortgage.ca

© 2024. All rights reserved - Matthew Maingot Mortgages

Matthew Maingot

Mortgage Agent Level 1

FSRA #M22002706

FSRA #13463