Did you get your mortgage in 2020? Pay close attention to your renewal date.

The Canadian housing market experienced an unprecedented boom in 2020, marked by record-breaking sales across the country. Increased real estate activity is positive for homeowners and investors, but it could result in higher payments for mortgage holders later on. As 2025 approaches, high sales volumes are worrying many Canadians about their financial stability. This blog post will examine the causes of payment shock and suggest strategies for homeowners to handle it.

REAL ESTATEHOUSINGONTARIOINTEREST RATESMORTGAGES

Matthew Maingot

6/2/20253 min read

The 2020 Real Estate Boom:

In 2020, the Canadian housing market saw a significant rise in sales due to low-interest rates, a demand for larger living spaces during the pandemic, and a preference for stable investments amid economic uncertainty. These conditions prompted many people to enter the market and purchase properties. However, the aftermath of this buying spree is now becoming evident.

Payment Shock and Rising Interest Rates:

The Bank of Canada's 2023 Financial System Review highlights rising worries about households' ability to manage their debt, especially for mortgage holders facing payment challenges. increases of up to 40% at renewal. The report indicates that financial pressure on households will likely rise as more mortgages are renewed in the coming years.

A significant contributing factor to payment shock is the potential rise in interest rates. Interest rates are currently low, but as the economy improves and inflation concerns grow, the Bank of Canada and other financial institutions may start to increase rates. This increase can greatly affect homeowners with adjustable-rate mortgages, leading to higher monthly payments and possible financial strain.

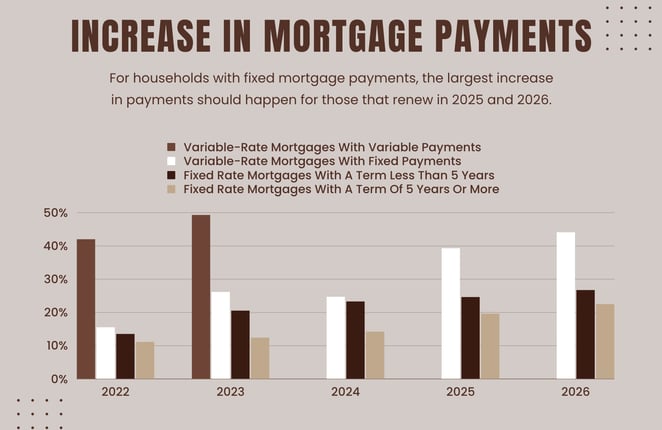

Expected Payment Increases at Renewals:

According to the Bank of Canada, around one-third of mortgages have already seen payment increases compared to February 2022. By the end of 2026, all mortgage holders are expected to see payment increases based on their mortgage type and previous rates.

For fixed-rate mortgages renewing in 2025-26, payments are projected to increase by 20% to 25%. Adjustable-rate borrowers have seen increases of over 50%, and variable-rate mortgage borrowers with fixed payments may need to raise their payments by about 40% to keep their original schedule if they renew in 2025 or 2026.

Comparing Mortgage Payments:

Let's compare the monthly mortgage payments for a $500,000 mortgage. In 2020, with a fixed interest rate of 1.79% for 5 years, payments would differ from those with a hypothetical interest rate of 4.79%. As you can see below, there is an increase of nearly $800 (+27%).

Please note that these figures are approximate and for illustrative purposes only. Actual mortgage payments may vary based on individual circumstances and market conditions. Rates are subject to change without notice.

How To Prepare For 2025-2026:

Schedule regular check-ups with your mortgage broker or lender to stay updated on market changes and find ways to optimize your mortgage. They can help you assess options like prepayment privileges or changing your payment frequency to match your financial goals.

Emergency Fund and Savings: Build and maintain an emergency fund to provide a buffer in case of unexpected financial challenges. Additionally, consider saving for future expenses or investment opportunities to enhance your financial resilience.

Debt Management: Evaluate your overall debt portfolio and explore strategies to manage and reduce high-interest debt. This may include debt consolidation, negotiating lower interest rates, or seeking professional debt counselling.

Maximize Home Equity: Regularly assess your home's value and explore ways to increase equity, such as home improvements or renovations. Building equity can provide additional financial flexibility and options in the face of payment shock.

In conclusion, proactive financial planning is crucial for mortgage holders to mitigate the impact of payment shock. Homeowners can effectively face challenges by reviewing mortgage agreements, budgeting, exploring refinancing, seeking professional help, and maximizing home equity. Engaging the services of a mortgage broker can provide valuable expertise and guidance throughout this process. With careful planning and informed decision-making, mortgage holders can safeguard their financial well-being and secure a stable future.

Growth

Empowering clients through personalized mortgage solutions.

Service:

info@matthewmortgage.ca

© 2024. All rights reserved - Matthew Maingot Mortgages

Matthew Maingot

Mortgage Agent Level 1

FSRA #M22002706

FSRA #13463